Brief Context

Context The Union Budget 2026–27 is expected to unveil a policy direction on the next phase of public sector bank (PSB) reforms based on two parallel tracks—Consolidation 2.0 and calibrated dilution of government ownership. What are the Reforms? Consolidation 2.0: The government is considering merging the five smallest PSBs with mid-sized banks with objectives to; To create banks with sufficient scale, balance sheet strength, and market presence.

Source Content

Syllabus: GS3/ Economy

Context

- The Union Budget 2026–27 is expected to unveil a policy direction on the next phase of public sector bank (PSB) reforms based on two parallel tracks—Consolidation 2.0 and calibrated dilution of government ownership.

What are the Reforms?

- Consolidation 2.0: The government is considering merging the five smallest PSBs with mid-sized banks with objectives to;

- To create banks with sufficient scale, balance sheet strength, and market presence.

- To reduce fragmentation in the PSB landscape.

- Ownership Reforms:

- FDI Limit Hike: Increasing the foreign direct investment (FDI) limit from 20% to 49%.

- Gradual Dilution: Reducing government stake closer to 51% to allow independent capital raising.

- Privatization: Renewing proposals to privatize two PSBs.

- Operational Autonomy: Granting more freedom to PSB boards.

Factors Propelling Performance of India’s Banks

- Asset Quality Review (AQR): Launched in 2015 compelled banks to recognize the true state of their loan books, bringing hidden NPAs to light and strengthening the supervisory framework.

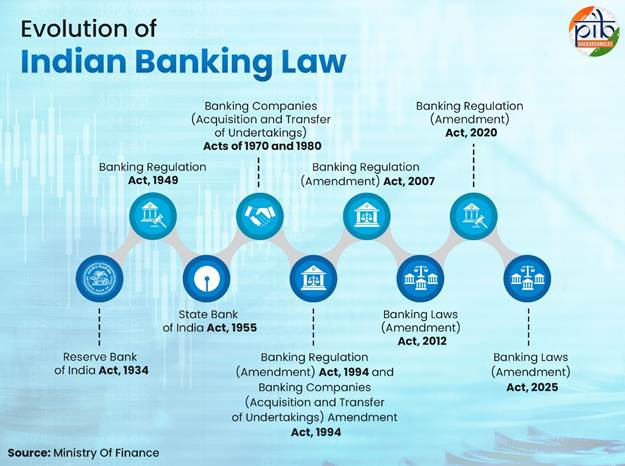

- Prompt Corrective Action (PCA) Framework: Helped restore the health of weak banks, followed by the consolidation of 27 PSBs into 12 by 2020.

- Insolvency and Bankruptcy Code (IBC): Introduced in 2016, along with complementary out-of-court resolution mechanisms, transformed India’s credit culture and improved recovery processes.

- Focused debt resolution: The pecuniary jurisdiction of Debt Recovery Tribunals (DRTs) was raised from ₹10 lakh to ₹20 lakh, enabling them to prioritize higher-value cases and improve recovery efficiency.

- RBI’s Prudential Framework for Resolution of Stressed Assets: Promotes early identification, reporting, and time-bound resolution of stressed loans, with incentives for lenders to act swiftly.

Challenges in India’s Banking Industry

- Hidden Stress in Loan Books: Despite lower headline NPAs, recoveries have not fully matched fresh slippages, particularly after pandemic-era restructuring.

- Basel III Transition: Large banks have strengthened capital buffers, but smaller banks face challenges in meeting capital adequacy, leverage, and liquidity norms.

- Financial Inclusion Constraints: Expansion into rural and underserved areas is constrained by gaps in digital literacy, connectivity, and financial awareness.

- Market Concentration Risks: Continued consolidation may reduce competition, potentially affecting customer choice, innovation, and efficiency in the long run.

Way Ahead

- Balanced Consolidation: Future mergers should prioritise complementary geographies, technology compatibility, and operational synergy rather than mere size expansion.

- Deepening Financial Inclusion: Investments in digital infrastructure, financial literacy, and last-mile connectivity are essential to convert access into meaningful usage.

- Cybersecurity Management: Enhanced supervisory oversight, stress testing, and cyber resilience frameworks are needed to safeguard financial stability.

Source: FE