Brief Context

Context Economic reforms in 2025 reflect a maturing phase of India’s governance, where the emphasis shifted decisively from “expanding regulatory frameworks” to “delivering measurable outcomes”. Income Tax Reforms The Union Budget 2025-26 exempted the annual incomes up to ₹12 lakh from income tax under the new regime, with the effective exemption rising to ₹12.75 lakh for salaried taxpayers on account of the standard deduction. The Government announced a comprehensive overhaul of the Income-tax

Source Content

Syllabus: GS3/ Economy

Context

- Economic reforms in 2025 reflect a maturing phase of India’s governance, where the emphasis shifted decisively from “expanding regulatory frameworks” to “delivering measurable outcomes”.

Key Reforms Shaping Growth and Opportunity

Income Tax Reforms

- The Union Budget 2025-26 exempted the annual incomes up to ₹12 lakh from income tax under the new regime, with the effective exemption rising to ₹12.75 lakh for salaried taxpayers on account of the standard deduction.

- The Government announced a comprehensive overhaul of the Income-tax Act, 1961, resulting in the New Income Tax Act, 2025.

- The Act strengthens digital-first enforcement, faceless tax administration, consolidates compliance provisions such as Tax Deducted at Source (TDS) under a single section etc.

Rural Employment Reforms

- Rural employment reforms anchored in the enactment of the Viksit Bharat – Guarantee for Rozgar and Ajeevika Mission (Gramin) Act, 2025, replacing the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA).

- Extended Employment Guarantee: 125 days of wage employment per rural household in a financial year.

- Strengthened Administrative Capacity: The administrative expenditure ceiling has been increased from 6% to 9%, strengthening staffing, training, technical capacity, and field-level support to improve institutional delivery and outcomes.

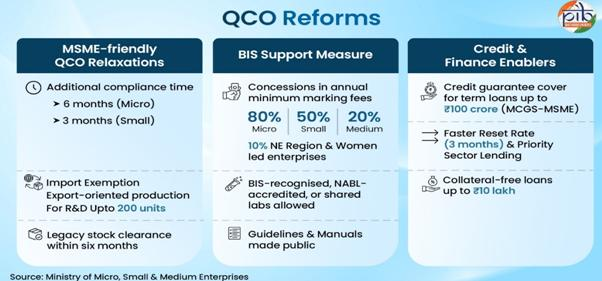

Ease of Doing Business Reforms

- To ensure that Quality Control Orders (QCOs) do not disrupt domestic production, the Government has implemented them in a phased and MSME-friendly manner through the Bureau of Indian Standards (BIS).

GST 2.0 Reforms

- Simpler Tax Structure: The move to a two-slab GST regime (5% and 18%) reduces complexity, classification disputes, and compliance costs.

- MSME and Startup Enablement: Faster refunds, simplified registration and returns, and lower input costs aim is to boost the present businesses and startups and incentivise the youth to enter into businesses and initiate startups.

- Wider Tax Base and Revenue Stability: Simpler rates and improved compliance have expanded the GST taxpayer base to over 1.5 crore, while gross collections reached ₹22.08 lakh crore in FY 2024–25, reinforcing fiscal sustainability.

Labour Reforms

- The Government of India consolidated 29 existing labour laws into four Labour Codes;

- The Code on Wages, 2019,

- the Industrial Relations Code, 2020,

- the Code on Social Security, 2020 and

- the Occupational Safety, Health and Working Conditions Code, 2020.

Export Promotion mission

- Announced in the Union Budget 2025–26, EPM marks a strategic shift from fragmented export support schemes to a single, outcome-based and digitally driven framework, aimed at empowering MSMEs, first-time exporters, and labour-intensive sectors.

Challenges Ahead

- Digital Divide: Digital-first governance in taxation, trade, and welfare delivery risks exclusion of smaller firms and workers lacking digital literacy or infrastructure.

- Global Economic Uncertainty: Sluggish global demand, geopolitical tensions, and supply-chain disruptions could limit export growth despite domestic reform momentum.

- MSME Compliance Burden: Despite simplification, smaller enterprises still struggle with digital compliance, quality standards, and access to affordable credit, particularly in semi-urban and rural areas.

- Centre–State Coordination: Reforms such as GST 2.0, labour codes, and rural employment require strong fiscal and administrative coordination, which continues to face operational frictions.

Way Ahead

- The reforms reflect a shift towards outcome-based governance, reducing friction for citizens and businesses, enhancing transparency, and laying the foundation for sustained, inclusive growth.

- The measures collectively foster trust, resilience, and global competitiveness in India’s economy.

Source: PIB