STATE OF THE ECONOMY

The Economic Survey Chapter 1 explains that global economy in 2024 is like a car stuck in traffic—some regions are moving ahead smoothly, while others face roadblocks. India, however, is navigating through the challenges efficiently, maintaining a steady pace of growth.

[Download Chapter 1 : Economic Survey (Official )]

Global Economic Overview

- The world economy is growing, but not evenly. Some regions like the U.S. are stable, while Europe and China are struggling.

- Inflation has cooled, but services remain expensive, making it tricky for central banks to decide on interest rates.

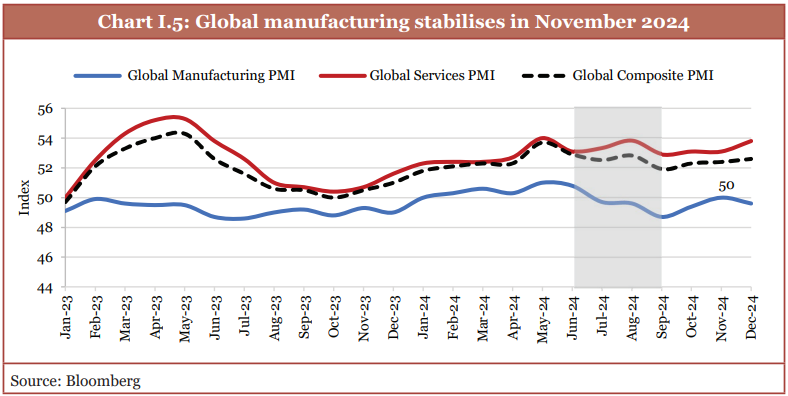

- Global manufacturing is slowing down, but services are doing well—especially in countries like India.

- Geopolitical risks, trade restrictions, and supply chain disruptions are adding uncertainty to global markets.

In this backdrop, India is expected to grow at 6.4% in FY25, despite pressures in manufacturing and external demand. The real strength of India’s economy is coming from:

✅ Agriculture, which has rebounded due to a strong Kharif harvest.

✅ Services, which continue to be the biggest contributor to growth.

✅ Private consumption, which remains strong despite global slowdowns.

✅ Government spending on infrastructure, which is keeping investments high.

But there are challenges too:

❌ Manufacturing is slowing down due to weak exports and seasonal effects.

❌ Inflation in food prices remains a problem, even though overall inflation is stable.

❌ Geopolitical and trade tensions can disrupt economic momentum.

The next sections dive deep into what’s driving India’s growth, what problems need to be solved, and what the future holds.

Global Economic Landscape in 2024

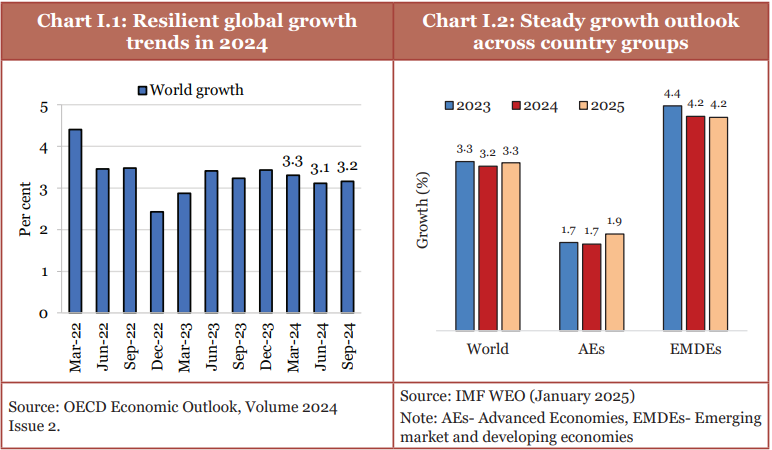

The world economy in 2024 is growing at 3.2%, as per the IMF projections, but that number hides big differences across regions.

United States: Steady Growth

- The U.S. economy is doing better than expected, with growth at 2.8% in 2024.

- Inflation has come down, but interest rates are still high, making borrowing expensive.

- Consumer demand is still strong, but signs of a slowdown are visible for 2025.

Eurozone: Struggling Performance

- The Eurozone is barely growing (0.8%), with Germany and Austria facing a manufacturing slump.

- France, Spain, and Poland are doing better, but overall, the region remains weak.

- Policy uncertainty in major economies like Germany is making investors nervous.

China: Decelerating Growth

- After a brief recovery, China’s economy weakened in Q2 2024, mainly due to:

- Low private consumption

- Real estate crisis

- Weak global demand for Chinese exports

- Growth is expected to slow further in 2025, making China less of a global growth driver than before.

Impact on India

✅ India benefits from U.S. and European demand for services (IT, finance, business services).

❌ But weak global demand affects India’s manufacturing exports, particularly steel, electronics, and chemicals.

❌ Trade policy changes, especially from the U.S. and Europe, could impact India’s exporters.

India's Economic Performance in FY25

India is growing at 6.4% in FY25, despite external uncertainties. Let’s break it down sector by sector.

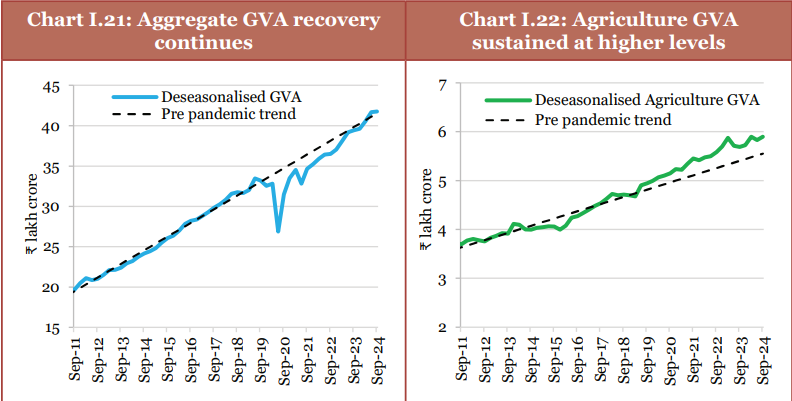

Agriculture Sector

- Growth rate: 3.8% in FY25 (higher than last year).

- Kharif food grain production: 1,647 lakh metric tonnes, 8.2% above the five-year average.

- Better monsoon and strong Rabi sowing mean agriculture will continue to support economic stability.

Why does this matter?

✅ Strong farm output = more income in rural areas = better demand for goods (bikes, FMCG, tractors, consumer products).

✅ Food inflation might reduce if supplies improve, which will help control overall inflation.

Challenges?

❌ Dependence on monsoon still remains a risk. If rainfall is unpredictable, the next crop cycle could be affected.

Industrial Sector

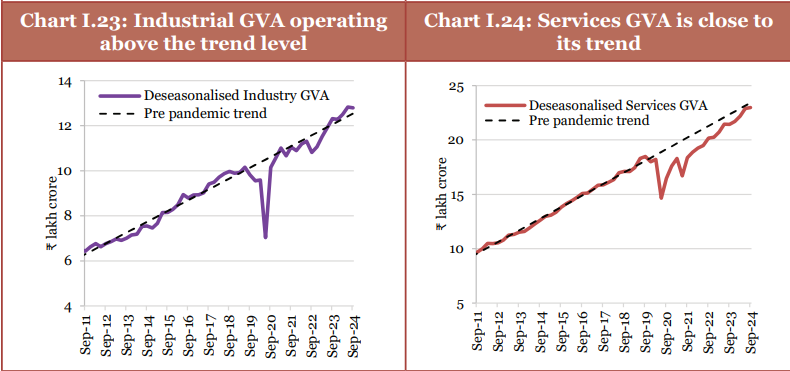

- Industrial growth: 6.2% in FY25 (lower than expected).

- Manufacturing is struggling due to weak exports, higher input costs, and sluggish global demand.

- Some key industries facing trouble:

- Steel: Prices have dropped due to oversupply in global markets.

- Cement: Demand slowed due to heavy rains and fewer construction projects.

- Oil & Refining: Companies faced inventory losses due to price volatility.

Why does this matter?

❌ Manufacturing needs to grow faster for job creation—it employs millions of people.

❌ Lower exports mean more pressure on domestic demand to drive economic growth.

Positives?

✅ Business expectations are improving, with stronger demand expected in Q3 and Q4.

✅ Government capex is helping the construction sector, which supports steel and cement demand.

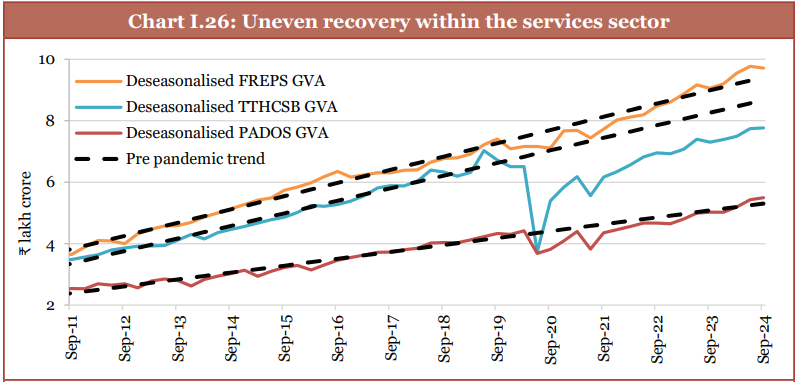

Services Sector

- Growth: 7.2% in FY25, making it the strongest sector.

- Major contributors:

- Financial services (banking, insurance, stock markets)

- Real estate and professional services

- IT and tech sector exports

Why does this matter?

✅ Services contribute the most to India’s GDP (over 50%).

✅ Strong global demand for Indian IT & business services helps sustain job creation and forex earnings.

Challenges?

❌ Higher costs of skilled labor could impact IT and business services competitiveness.

Investment Trends and Inflation Dynamics

Investment Trends

Investment plays a crucial role in sustaining economic momentum by driving infrastructure development, enhancing industrial capacity, and generating employment. In FY25, India’s investment trends have shown a mixed picture, with strong government spending but cautious private sector participation.

🔹 Government Capital Expenditure (Capex):

- Government capex grew by 8.2% in FY25, with heavy investments in infrastructure projects like roads, railways, power, and defense.

- The government’s focus on large-scale infrastructure development aims to improve connectivity, reduce logistical costs, and enhance trade efficiency.

- Increased spending on highways, metro projects, and renewable energy has created employment opportunities and supported construction activity.

- Public sector investment acts as a catalyst for private sector confidence, encouraging industries to expand operations.

🔹 Private Investment Trends:

- Private sector investment remains slow due to global uncertainty, high interest rates, and weak export demand.

- However, there are early signs of recovery—order books of capital goods companies expanded by 23.6% in FY24, indicating upcoming private investment growth.

- Capacity utilization in manufacturing has increased to 74.7%, suggesting that companies may soon ramp up production and capital spending.

- The Make in India initiative, PLI (Production-Linked Incentive) schemes, and corporate tax reductions continue to provide incentives for private investments.

- A revival in consumer demand and stability in input costs could further encourage businesses to increase investments in machinery, factories, and expansion projects.

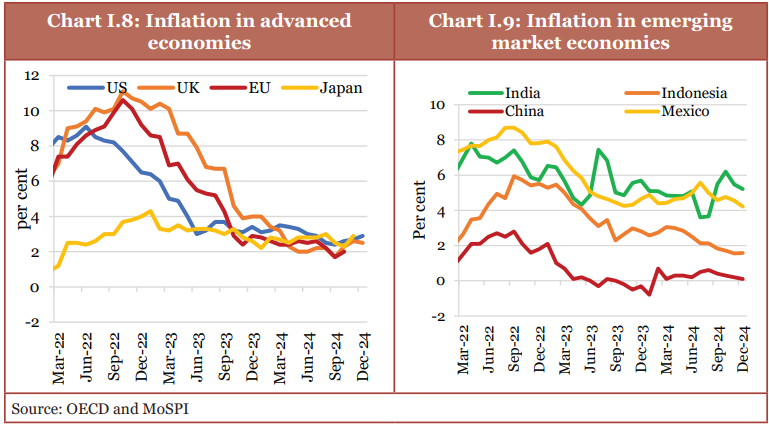

Inflation Dynamics

While overall inflation has remained within the Reserve Bank of India’s comfort range, food inflation continues to pose challenges. A rise in vegetable and pulse prices has affected household budgets, particularly in rural areas, where food expenses make up a larger share of overall spending.

🔹 Consumer Price Index (CPI) Trends:

- Overall inflation (CPI) averaged 4.9% between April-December 2024, staying close to the RBI’s target of 4%.

- Core inflation (which excludes food & fuel) has declined to 4.5%, indicating stable prices in non-food sectors.

- Food inflation surged to 8.4%, largely driven by high prices of vegetables and pulses due to weather-related supply disruptions and seasonal effects.

🔹 Why This Matters:

✅ Lower core inflation is good for businesses and households, as it provides price stability in services, housing, and transportation.

❌ High food inflation impacts household consumption, reducing disposable income and affecting demand for other goods.

❌ Volatile food prices create uncertainty, making it harder for policymakers to predict inflation trends and set interest rates.

✅ Better agricultural output and government price controls may help ease food inflation in the coming months.

External Sector Resilience and Challenges

India’s external sector has remained resilient despite global trade uncertainties, supply chain disruptions, and currency fluctuations. The trade balance, foreign exchange reserves, and remittances have provided stability, but challenges in global trade and investment flows remain a concern.

🔹 Exports & Trade Balance:

- India’s merchandise exports grew by 1.6% between April-December 2024, supported by stronger demand in key markets.

- Services exports (IT, business services, and financial services) continue to perform well, making India one of the top 7 global services exporters.

- Imports grew by 5.2%, led by demand for oil, gold, and electronic goods, which widened the trade deficit.

- The weakening of global demand for goods like textiles, chemicals, and auto components has

🔹 Foreign Exchange Reserves:

- India’s foreign exchange reserves stood at a comfortable level of USD 620 billion as of end-December 2024, providing a strong buffer against external shocks.

- The reserves cover approximately 10 months of projected imports, indicating robust external sector stability.

🔹 Current Account Deficit (CAD):

- The Current Account Deficit (CAD) is projected to remain manageable, financed by robust capital inflows.

- Despite the widening trade deficit, strong services exports and resilient remittances have helped contain the CAD.

🔹 Capital Flows & Remittances:

- Foreign Direct Investment (FDI) inflows remained robust, reflecting investor confidence in India’s long-term growth prospects.

- Foreign Portfolio Investment (FPI) witnessed volatility but net inflows remained positive, supported by India’s strong macroeconomic fundamentals.

- Remittances from overseas Indians continued their strong growth trajectory, providing a significant and stable source of external financing.

Fiscal Developments and Public Finance

The government’s fiscal policy has focused on prudent management, capital expenditure-led growth, and fiscal consolidation. Despite global uncertainties, tax revenues have shown buoyancy, supporting public investment and social sector spending.

🔹 Revenue Receipts:

- Gross Tax Revenue registered a growth of 11.5% during April-December 2024, driven by robust GST collections and direct tax buoyancy.

- GST collections consistently surpassed the INR 1.7 lakh crore mark, reflecting formalization of the economy and improved compliance.

- Non-tax revenues also performed well, contributing to overall revenue growth.

🔹 Expenditure Trends:

- The government maintained its focus on capital expenditure, which grew by 25% during the first three quarters of FY25, boosting infrastructure creation and crowding in private investment.

- Revenue expenditure was managed prudently, with targeted spending on social welfare schemes and subsidies.

🔹 Fiscal Deficit & Public Debt:

- The fiscal deficit is on track to meet the budgeted target, demonstrating the government's commitment to fiscal consolidation.

- Public debt-to-GDP ratio has shown a declining trend, supported by strong nominal GDP growth and prudent debt management strategies.

Social Infrastructure and Human Development

India has made significant strides in enhancing social infrastructure and human development, with continued focus on education, health, and employment generation. Government initiatives aim at inclusive growth and improving the quality of life for all citizens.

🔹 Education:

- Gross Enrolment Ratio (GER) at all levels of education has improved, with notable progress in higher education and vocational training.

- The National Education Policy (NEP) 2020 is being implemented to transform the education sector, focusing on skill development and future-ready learning.

🔹 Health:

- Public health expenditure as a percentage of GDP has increased, with greater emphasis on primary healthcare.

- Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) has expanded its coverage, providing health insurance to a large segment of the population.

- Significant progress has been made in vaccination drives and maternal & child health indicators.

🔹 Employment & Poverty Reduction:

- The Periodic Labour Force Survey (PLFS) data indicates a decline in the unemployment rate and an increase in the Labour Force Participation Rate (LFPR), particularly for women.

- Government schemes like MGNREGA and PM SVANidhi continue to support rural employment and urban livelihoods.

- Efforts to reduce multi-dimensional poverty have yielded positive results, lifting millions out of poverty through targeted interventions.

Outlook and Policy Priorities

India's economy is poised for continued robust growth, driven by strong domestic demand, public capital expenditure, and structural reforms. While global uncertainties persist, India's macroeconomic stability and policy agility provide a strong foundation. The government's policy priorities will continue to focus on:

- Sustaining high growth with macroeconomic stability.

- Boosting manufacturing and exports through PLI schemes.

- Furthering ease of doing business and attracting FDI.

- Investing in human capital and social infrastructure.

- Accelerating green transition and climate action.

1. Based on the provided text, which of the following statements about India's external sector is correct?

Correct Answer: d) Services exports make India one of the top 7 global services exporters.

2. Which of the following factors contributed to the widening of India's trade deficit as per the Economic Survey?

Correct Answer: c) Increased demand for gold and electronic goods.

Source: LearnPro Editorial | Economy | Published: 1 February 2025 | Last updated: 12 March 2026

About LearnPro Editorial Standards

LearnPro editorial content is researched and reviewed by subject matter experts with backgrounds in civil services preparation. Our articles draw from official government sources, NCERT textbooks, standard reference materials, and reputed publications including The Hindu, Indian Express, and PIB.

Content is regularly updated to reflect the latest syllabus changes, exam patterns, and current developments. For corrections or feedback, contact us at admin@learnpro.in.